Please check back regularly for an updated listing of all of Bob’s live webinars and conferences. Please follow the links provided for additional details on each event and information on how to register/attend!

Thursday October 03, 2024 4:00 PM EST - 5:30 PM EST

Managing Capital Gains in 2024

In this class Bob Keebler will review the following:

- The use of charitable remainder trusts to defer and eliminate capital gains

- The use of § 453 installment sales to reduce capital gains and how to elect out of installment sale treatment to accelerate gains into 2025

- The Math of recognizing capital gains in 2024

- Grantor charitable lead trusts to decrease capital gains

- Direct charitable gifts to reduce capital gains

- Opportunity zones to more effectively manage capital gains

- Integrating loss harvesting in an overall capital gains strategy

- Using 1031 exchanges to ease capital gains

- The use of collars, variable forward sales and options to better manage capital gains

- IRC § 1259 ?choking? collar to trigger capital gains in 2024 or defer to a future date

- Short against the box? strategies to choose between recognizing gains in 2024 or 2025

Friday October 04, 2024

Understanding the IRS's Final Regulations on Required Minimum Distributions

Join Bob Keebler as he reviews all of the issues you need to be on top of, including:

Wednesday October 09, 2024 11:00 AM EST - 12:30 PM EST

Maximizing Wealth with SLATs and Sunset Strategies

Because of Sunset, Spousal Lifetime Access Trusts have become one of the most commonly-used and powerful planning techniques in the planner’s toolbox. In his exclusive LISI Webinar, Bob Keebler, CPA/PFS, AEP (Distinguished), will give you all you need to know about on planning with SLATs, including:

- Understanding the key components of a SLAT, how they work and why they’re used

- Learn how the Reciprocal Trust Doctrine works and how to avoid it

- Why SLATs are efficient even for clients who won’t be subject to the estate tax, and more importantly, even when the unified credit is cut in half

- Why is it important to mix and match techniques like SLATs, DAPTs, hybrid DAPTs, and SPATs to get the best results for your clients?

- Understanding when a SLAT is taxed versus being disregarded and when to “toggle off” grantor tax status

- What are the most critical considerations for ensuring that clients maintain control/access to their trust assets

- Commons traps for the unwary in these commonly used trusts

- Common risk management and compliance issues that must be considered when using these trusts with clients

- Choosing the right situs and trustee

- Funding considerations and asset protection considerations

- Critical case studies that demonstrate all of the concepts mentioned above

Who should take this class? CPAs, attorneys, financial planners and other professional financial planners who regularly deal with estate planning, tax and retirement planning issues.

Thursday October 10, 2024 12:00 PM EST - 1:30 PM EST

Understanding the IRS's Final Regulations on Required Minimum Distributions

Join Bob Keebler as he reviews all of the issues you need to be on top of, including:

Tuesday October 22, 2024 2:00 PM EST - 3:30 PM EST

Maximizing Wealth with SLATs and Sunset Strategies

Because of Sunset, Spousal Lifetime Access Trusts have become one of the most commonly-used and powerful planning techniques in the planner’s toolbox. In his exclusive LISI Webinar, Bob Keebler, CPA/PFS, AEP (Distinguished), will give you all you need to know about on planning with SLATs, including:

- Understanding the key components of a SLAT, how they work and why they’re used

- Learn how the Reciprocal Trust Doctrine works and how to avoid it

- Why SLATs are efficient even for clients who won’t be subject to the estate tax, and more importantly, even when the unified credit is cut in half

- Why is it important to mix and match techniques like SLATs, DAPTs, hybrid DAPTs, and SPATs to get the best results for your clients?

- Understanding when a SLAT is taxed versus being disregarded and when to “toggle off” grantor tax status

- What are the most critical considerations for ensuring that clients maintain control/access to their trust assets

- Commons traps for the unwary in these commonly used trusts

- Common risk management and compliance issues that must be considered when using these trusts with clients

- Choosing the right situs and trustee

- Funding considerations and asset protection considerations

- Critical case studies that demonstrate all of the concepts mentioned above

Who should take this class? CPAs, attorneys, financial planners and other professional financial planners who regularly deal with estate planning, tax and retirement planning issues.

Approximately the third week of the month

The Robert Keebler Tax & Estate Planning Monthly Bulletin

There have been changes in estate, tax, income, and retirement planning laws coming for a while now and it is more imperative than ever for estate planners to stay on top of these changes. Includes: Monthly bulletin sent via e-mail (approximately the third week of the month). Subscribe for $49 per month.

Downloadable E Book

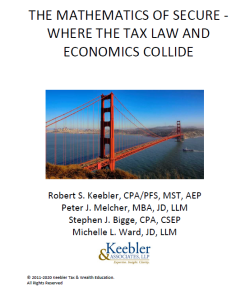

The Secure Act E-Book: “The Mathematics of the SECURE Act: Where Tax Law and Economics Collide”

Most estate planning professionals are already very well aware that the SECURE Act brought with it some of the biggest changes to IRA planning for clients than we have seen during our lifetime. That’s why it’s so important as estate planners that we have what we need to understand the SECURE Act and what you need to know to properly advise your clients.

This is why we, as we have in the past, have teamed up with nationally renowned CPA and IRA expert, Robert S. Keebler, to break it down for you so that you don’t have to do it yourself. Subscribe to the Printable EBook. (Includes: Downloadable, printable PDF e-Book. Pages 108.)